May numbers show the San Diego and North County housing markets continuing the same pattern we’ve seen throughout the spring. Inventory remains limited, prices are holding steady, and higher mortgage rates have not yet had a significant impact on local housing activity.

Altos Research continues to classify single-family homes as a strong seller’s market while condos remain in slight seller’s territory. At the higher end of the market, pending sales of multimillion-dollar homes increased in May, according to a recent San Diego Union-Tribune report.

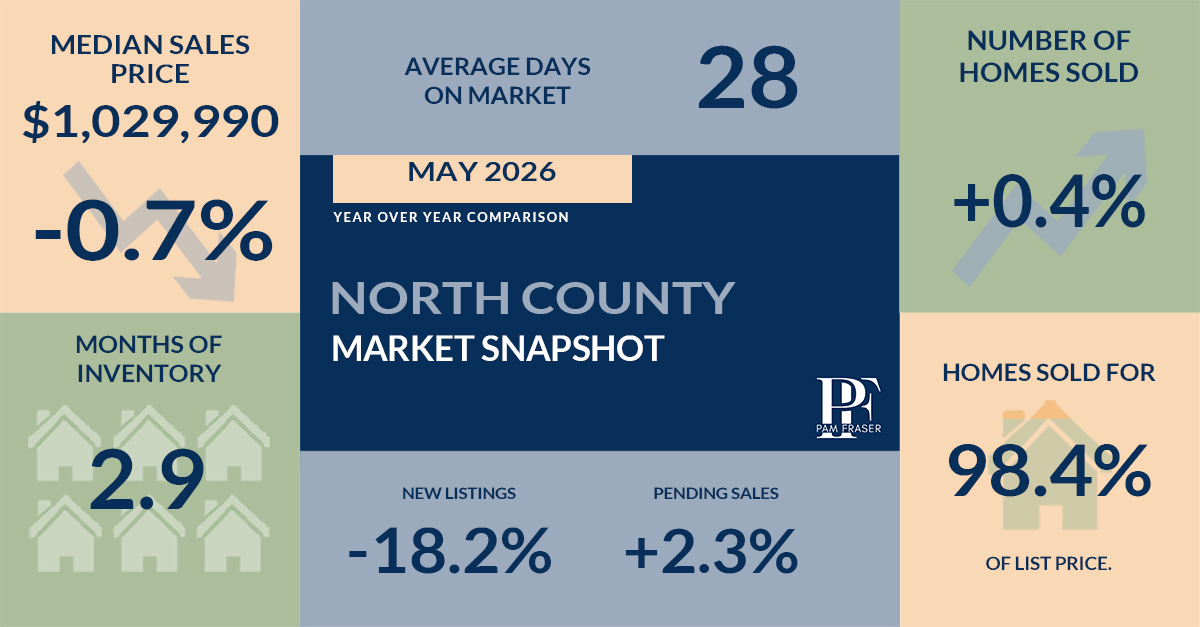

The countywide median sales price was $925,000 in May, exactly the same as it was two years ago. In North County, the median price was $1,029,990, slightly below both May 2024 and April 2026 levels. Although inventory is higher than it was two years ago, it remains below long-term norms. With supply still limited, prices have remained remarkably stable despite higher mortgage rates and concerns about inflation.

Below are answers to some of the most common questions about current market conditions.

San Diego Housing Market FAQs

Are home prices rising in San Diego County?

Countywide, the median home price was $925,000 in May. That is exactly where prices were two years ago. In North County, the median price was $1,029,990, lower than May 2024 and slightly below April’s level.

What is happening with inventory?

Inventory remains limited. Active listings are down 12.4 percent year over year countywide and nearly 30 percent in North County. Supply increased slightly month over month but remains below long-term norms.

Are homes taking longer to sell?

No. Countywide days on market remained at 33 days, unchanged from one year ago. In North County, days on market increased slightly from 26 to 28 days.

Are sales increasing?

Sales activity remains relatively stable. The number of homes sold was very close to last year’s level, reflecting both limited inventory and many buyers remaining on the sidelines.

Is this still a seller’s market?

Yes. Altos Research continues to classify single-family homes as a strong seller’s market, while condos remain in slight seller’s territory. Limited supply continues to support pricing, though buyers remain selective.

Looking for more detail or wondering what your home is worth in today’s market? Request a free home valuation.

Interest Rates

Below are current mortgage rate averages and recent changes, updated regularly.

Market Updates

Click on the links below to read the San Diego real estate market reports.

- NORTH COUNTY MONTHLY INDICATORS

- METRO SAN DIEGO COUNTY MARKET UPDATE

- EAST SAN DIEGO COUNTY MARKET UPDATE

- SOUTH SAN DIEGO COUNTY MARKET UPDATE

- SAN DIEGO COUNTY MONTHLY INDICATORS

- 2025 SAN DIEGO COUNTY MARKET REPORT

North County Housing Summary

Here’s how the North County market performed compared to last year.

- Median home prices declined 0.7 percent.

- Detached home prices decreased 9.5 percent, from $1,248,997 to $1,130,000.

- Sold units increased 0.4 percent. Pending sales grew 2.3 percent.

- Median days on market increased to 28, up 7.7 percent from last year.

- Months of inventory decreased from 4.9 months to 2.9 months.

San Diego County Housing Summary

Here are the numbers for San Diego County.

- Median prices rose 1.3 percent, from $913,500 to $925,000.

- Detached home prices were unchanged at $1,099,500.

- Attached home prices decreased 1.5 percent to $675,000.

- Months of inventory decreased from 3.5 months to 3.0 months.